Why the future of Fintech belongs to industry-specific financial tools

Published on Apr 14, 2026

Investment Thesis

Must-Read

Our team has spent a decade watching the fintech space evolve. The first wave was about accessibility, with Stripe and QuickBooks making payments and ledgers easier to use. The second wave focused on convenience, with companies like Brex, Ramp, and Stampli reimagining financial infrastructure for startups and SMBs by offering corporate cards, expense management, bill pay, and real-time spend controls that legacy banks had long neglected.

For SaaS businesses with simple invoices and predictable revenue, these fintech offerings work well. But for the rest of the $35 trillion economy, building skyscrapers, dispensing life-saving meds, and producing streaming hits, horizontal fintech misses the mark entirely.

Here's what’s often overlooked: operators in these industries don't think of payments as a standalone workflow.

A pharmacy dispensing a prescription triggers a chain of reimbursement claims, DIR fee exposure, insurance receivable aging, and cash flow forecasting amid retroactive clawbacks.

An HVAC contractor swiping a card for materials is just the start, as that purchase flows into job costing, vendor term management, and seasonal cash planning.

A construction subcontractor doesn’t send invoices, but instead submits Application and Certificate for Payment applications (AIA G702), in which 5-10% of each payment is withheld for a period of months.

In these businesses, payments drive downstream decisions like what to collect, when to extend credit, and how to forecast. Solving only the payments piece, while ignoring everything around it, actually makes outcomes worse. What customers need is an integrated solution that spans the full cycle from billing to collections, with payments as one step in a connected process.

These aren't edge cases. They're major industries with financial workflows so structurally distinct that generic tools create real revenue gaps. Advancements in AI have now made it economically viable to build for specific industries, not by bolting a payments tab onto vertical software, but by making the financial layer native to how each industry actually operates.

We’re seeing this firsthand with our portfolio companies. For example,Affiniti started with co-branded business credit cards for independent pharmacies, and then expanded into trades and health clinics. They’re now a full-stack financial operating system tailored to each vertical’s actual cash flow mechanics. Their wedge wasn’t just about better bookkeeping, but about understanding that a pharmacy’s P&L looks nothing like an HVAC shop’s or a podiatry clinic’s, and then they built financial products focused on those unique differences.

Their success validated our conviction that winning in fintech today is about solving deep industry problems versus taking a horizontal approach.

Defining the category: The 4 pillars of Vertical AI Fintech

To be clear, we're not interested in standalone vertical payments, but rather in vertical end applications where payments are one way they monetize, while the real value lies in owning the entire financial workflow—from billing through collections and everything downstream.

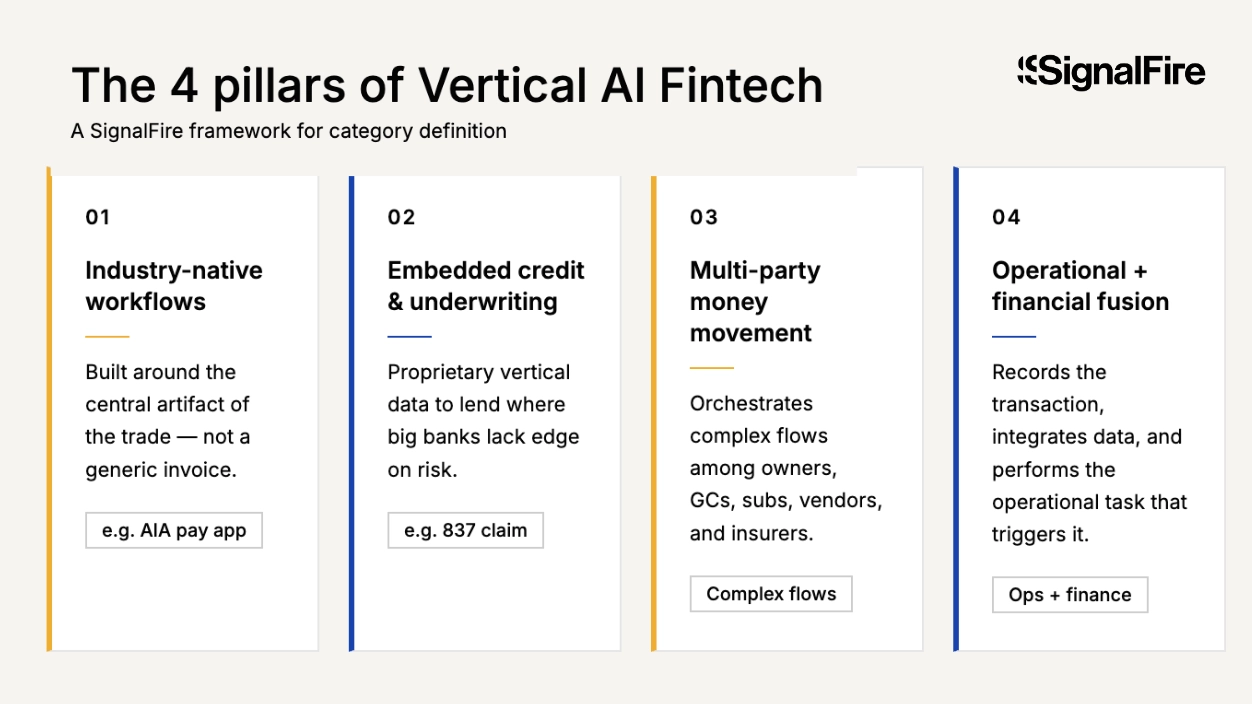

At SignalFire, we define Vertical AI Fintech by four specific traits:

Industry-native workflows: The product and platform are built around the central artifact of the trade (e.g., an AIA pay app or an 837 healthcare claim), not a generic invoice.

Embedded credit and underwriting: The company uses proprietary, vertical data to lend to industries where a big bank wouldn't have the edge to clearly see the risk.

Multi-party money movement: The product orchestrates complex money flows among owners, GCs, subs, vendors, and insurers.

Operational + financial fusion: The software doesn't just record the transaction, but also integrates financial data and performs the operational task that triggers it. Payments feed decisions downstream: w hat to collect, when to underwrite, how to forecast.

The three market shifts that unlocked this wave

Industry demand for tailored financial tools isn’t new, but previously, messy data, poor unit economics, and immature infrastructure held back innovation.

Three recent market shifts are making this wave possible today:

AI makes messy data usable: AI can finally read and digest the thousands of unstructured GC billing formats or opaque PBM reimbursement rules that previously required an army of back-office humans.

Vertical software is cheaper to build: New development tools are enabling the creation of world-class financial OS platforms across diverse sectors, such as pharmacies and distributors.

The infrastructure has matured: BaaS and embedded rails are now table stakes, and the value has shifted from having a bank partner to having the best logic layer sitting atop those rails.

The 3 frontier verticals for industry-native Fintech

Here are three verticals where horizontal fintech fundamentally breaks down, and where vertical AI is creating the next generation of financial infrastructure:

1. Construction – The war on retainage

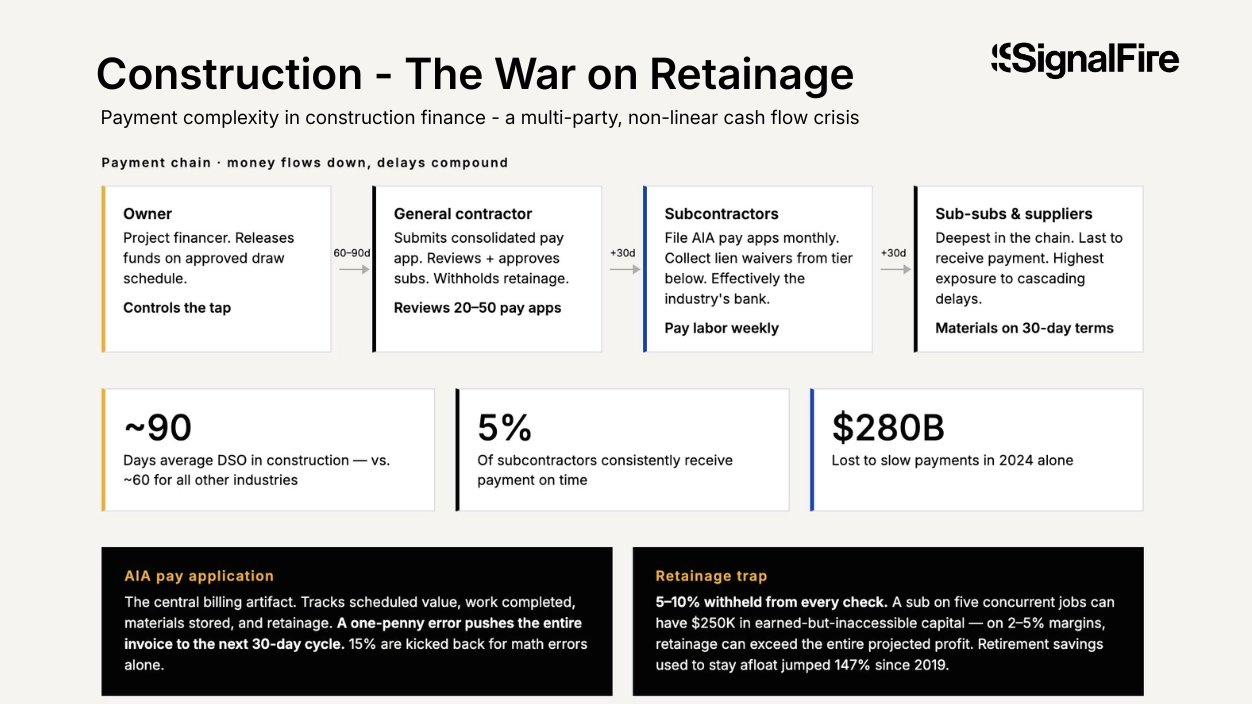

Construction finance is structurally challenging because cash flow is non-linear and flows through a multi-party chain: from the owner to the general contractor (GC) to subcontractors, sub-subcontractors, and material suppliers.

A large commercial project can have 20-50 subcontractors, each submitting their own pay applications, collecting lien waivers from the tier below, and waiting for the tier above to approve and pay them. Subcontractors effectively act as the industry's bank, paying for labor weekly and materials on 30-day terms, but waiting 60-90+ days for their payment.

The industry’s average DSO runs ~90 days, versus ~60 for all other industries. Only 5% of subcontractors consistently receive payments on time.

The point of friction: The central billing artifact is the AIA pay application, a cumulative, progress-based invoice that tracks each line item’s scheduled value, work completed, materials stored, and the retainage withheld. Even a one-penny error can push the whole invoice to the next billing cycle, delaying payment by 30 days. On average, 15% of pay applications are kicked back for math errors alone.

The key pain point: The retainage withheld is typically 5–10% of every check,so a subcontractor running five concurrent projects might have $250,000 in “earned but inaccessible” capital at any time. On an already thin 2–5% margin, retainage can exceed the entire projected profit on a job. This explains why the rate at which subcontractors use retirement savings to stay afloat has jumped 147% since 2019. Then there are lien waivers, prevailing wage requirements covering ~$217 billion in annual public construction spending, and change orders that affect every downstream financial document. The industry lostan estimated $280 billion to slow payments in 2024 alone.

The AI unlock: QuickBooks can’t generate an AIA form, track retainage, produce certified payroll, or run a WIP report. It wasn’t built to do these things. Startups like Siteline have digitized 23,000+ pay app and lien waiver forms from 17,000+ GCs, enabling one-click generation in each GC’s exact format, helping customers get paid weeks faster. Another startup, Constrafor, enables subcontractors to get paid within 24-48 hours, improving cash flow cycles by up to 85 days. AI enables auto-generating pay applications, predicting which GCs pay fastest, modeling retainage accumulation and release timelines per project, and flagging compliance violations in real time.

2. Film & television production

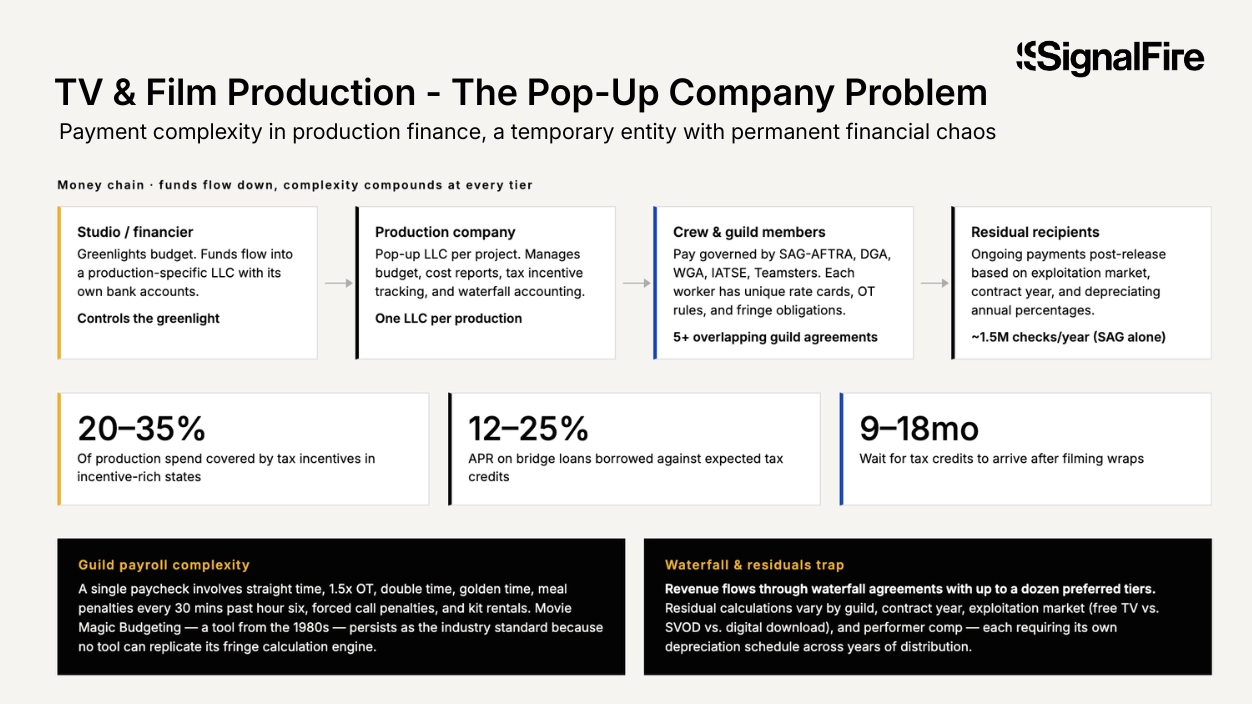

Every film or TV production is a temporary, pop-up company with its own bank accounts and payroll, and financial complexity that would break any horizontal tool.

The point of friction: Let’s start with payroll. A single crew member’s pay calculation involves straight time, overtime at 1.5x, double time, golden time, meal penalties every 30 minutes past the sixth hour, forced call penalties, kit rentals, and mandatory pension/health contributions, all governed by overlapping rules from SAG-AFTRA, DGA, WGA, IATSE, and the Teamsters. After the project wraps, residual payments kick in: SAG-AFTRA alone processes ~1.5 million residual checks per year, each calculated based on guild, contract year, exploitation market (domestic free TV vs. SVOD vs. digital download), performer compensation, and depreciating annual percentages.

The key pain point: Tax incentives account for 20-35% of production spend in incentive-rich states. Productions borrow against expected credits at 12-25% APR through bridge loans since credits typically arrive 9-18 months post-filming. Revenue flows through waterfall agreements, with up to a dozen preferred tiers to account for.

Movie Magic Budgeting, an archaic, cumbersome tool from the 1980s, persists as the industry standard because no horizontal tool can replicate its fringe calculation engine. Wrapbook is an example of what vertical-native fintech looks like here: purpose-built payroll that actually understands guild rules, tax incentive tracking, and production-specific accounting.

The AI unlock: AI can accelerate this whole process by automating residual calculations across multiple guild agreements, optimizing tax-incentive stacking across 100+ global programs, and generating real-time cost reports that previously required days of manual reconciliation.

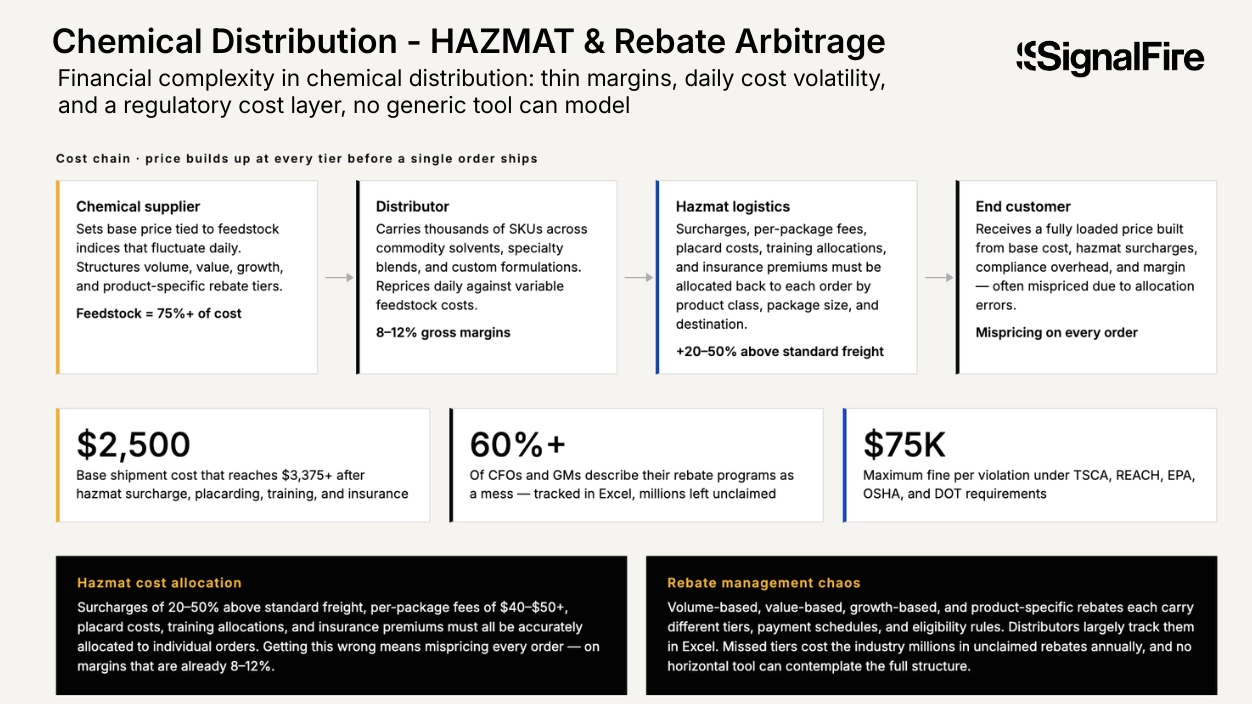

3. Chemical distribution - HAZMAT & rebate arbitrage

The chemical and chemical distribution industries operate on tight gross margins of 8–12% while navigating one of the most complex pricing environments in manufacturing. Yet most chemical companies still rely on3 spreadsheets and analyst intuition to set prices—even though variable costs like feedstock, which fluctuate daily, make up more than 75% of total product cost.

The point of friction: A single distributor might carry thousands of SKUs across commodity solvents, specialty blends, and custom formulations, each with different cost structures, shelf-life constraints, and potency-based inventory valuation.

Hazmat logistics add a structural cost layer that generic tools can’t model. Surcharges of 20%-50% above standard freight, per-package fees of $40-$50+, placard costs, training allocations, and insurance premiums, all of which must be accurately allocated back to individual customer orders across different product classifications, package sizes, and destinations.

A base chemical shipment costing $2,500 can reach $3,375+ after hazmat surcharge, placarding, training allocation, and insurance are applied. Getting this allocation wrong means mispricing every order and losing profits.

The key pain point: Rebate management is where the most money is left on the table. Over 60% of CFOs and GMs in the industry describe their rebate programs as a mess. Chemical suppliers commonly structure volume-based, value-based, growth-based, and product-specific rebates, each with different tiers, payment schedules, and eligibility rules. Distributors still largely track them in Excel, and missed tiers cost the industry millions in unclaimed rebates. Layer on regulatory compliance costs (TSCA, REACH, EPA, OSHA, DOT requirements carrying $10,000 to $75,000 in fines per violation), and you have an industry where the financial workflow is deeply intertwined with operational and regulatory complexity in ways no horizontal tool can contemplate.

The AI unlock: No pure-play vertical fintech startup has meaningfully addressed this space. AI can enable dynamic pricing that ingests real-time feedstock indices across thousands of SKUs, rebate optimization that tracks progress against all supplier tiers simultaneously, automated hzmat cost allocation to specific products and customers, and regulatory compliance cost tracking at the lot level. For a margin-constrained industry, even a 50-basis-point improvement in pricing or rebate capture is transformative.

Other verticals ripe for industry-native Fintech:

Healthcare clinics (including veterinary)

Auto & vehicle services

Logistics & freight brokerage

Professional services

Food & beverage distribution

Building the new financial layer

The opportunity is the same across all these verticals: industries with complex, multi-party, or irregular financial flows that horizontal tools were never designed to support. The winners in this space won’t be fintech companies that bolt onto existing horizontal tools, but vertical AI companies that treat the financial layer as the product itself, built around how each industry actually moves money.

If you’re building vertical financial infrastructure for an underserved industry, we’d love to hear from you. Email Varun at varun@signalfire.com or Jon at jon@signalfire.com.

*Portfolio company founders listed above have not received any compensation for this feedback and may or may not have invested in a SignalFire fund. These founders may or may not serve as Affiliate Advisors, Retained Advisors, or consultants to provide their expertise on a formal or ad hoc basis. They are not employed by SignalFire and do not provide investment advisory services to clients on behalf of SignalFire. Please refer to our disclosures page for additional disclosures.

Subscribe to our newsletter

We typically send no more than 4-6 newsletters/yr with helpful tips on company building, our perspectives on industry trends, and event invites.

Moats are for castles: A new argument for permanence over defensibility in AI startups

Stop manufacturing premature moats. This post argues that AI startups should prioritize permanence over defensibility. Learn why real moats are earned by solving persistent problems that endure even when intelligence is a cheap commodity. (188 characters)

Read more

Sales & Go-to-Market

Must-Read

Practitioner’s Perspective

April 29, 2026

Build or buy? Navigating the new era of GTM AI Agents

Build vs. buy for GTM agents? After a year building custom sales and RevOps agents at Together AI and Resolve AI, two operators share the heuristic that actually works, plus four real examples, what they cost, and where to start Monday.

Read more

Must-Read

Practitioner’s Perspective

March 9, 2026

Beyond the billable hour - How AI is reshaping margins and models at law firms

A deeper look at how AI is changing the billable hour, law firm margins, and legal pricing models. Here's why flat fees, subscriptions, and hybrid pricing are gaining traction.

Read more

Data Reports

Beacon AI

February 4, 2026

Unicorn DNA — Where today’s billion-dollar startup founders come from

A data-driven analysis of 2,000+ founders behind 800 U.S. unicorns reveals where billion-dollar founders come from, why experience beats hype, how AI is reshaping the founder pipeline, and how top engineering schools are outpacing the Ivy League.

Read more

Must-Read

Investment Thesis

AI/ML

December 2, 2025

The built economy: How vertical AI is unlocking the biggest untapped market in trades and construction

Construction, HVAC, plumbing, electrical, and remodeling businesses are being transformed by AI. See how vertical AI cuts admin time, speeds estimating, automates proposals, and modernizes field operations.

Read more

Portfolio

Investment

February 18, 2026

The missing layer in Enterprise AI: Why we invested in Solid

Solid raises $20M to solve enterprise AI’s context problem, building a trusted semantic layer that makes AI agents accurate, reliable, and production-ready.

By clicking “Accept”, you agree to the storing of cookies on your device to enhance site navigation, analyze site usage, and assist in our marketing efforts. View our Privacy Policy for more information.